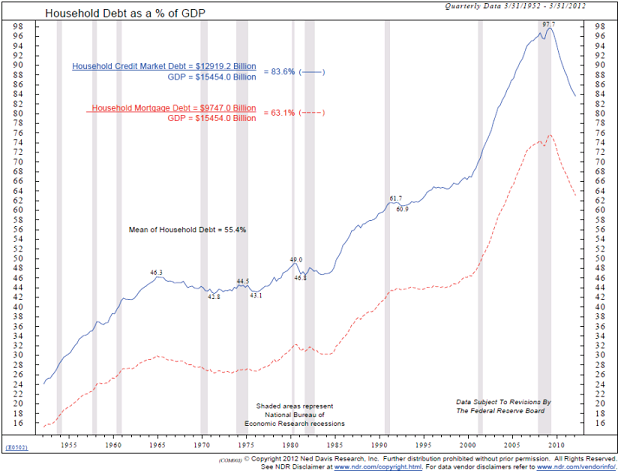

In our view, it is the overwhelming force of the debt deleveraging that has overcome government efforts to inflate. We have pointed out that household debt has dropped to 84% of GDP from its peak of 98% in 2008. After rising for 284 consecutive quarters from the end of WW II to mid-2008, household debt has now declined for the last 16 quarters. This is an astounding number, indicating a great change in the economy. It still has a long way to go in order to reach the 66% level of 2000, let alone the 60-year average of 55%. Households, therefore, have to continue to increase savings and reduce spending for, perhaps, years to come to get their balance sheets in order. Since this reduces the demand for goods and services, businesses have little reason to hire new workers or increase capital expenditures. Since household spending accounts for 70% of the GDP, the negative effects are felt throughout the economy. (emphasis mine)Read it at Pragmatic Capitalism

DEFLATION REMAINS A BIGGER THREAT THAN HIGH INFLATION

By Comstock Partners

Over the past couple weeks, I have seen an increasing number of people argue that the private sector may be approaching levels of debt where credit expansion can once again begin in earnest. While countless others focus on the size of public debt, which is somewhat irrelevant for the US, the primary cause of the Great Recession and mediocre economy today was/is excessive household debt.

Unlike the US government, households cannot print money to repay their debts and therefore must rely on either income, savings or new borrowing. In the final stage of a bubble, termed “Ponzi finance” by Minsky, the last of these methods becomes the primary means of refinancing outstanding debt. When credit conditions eventually tightened, many households were forced to reduce consumption in order to repay previous debts. Unfortunately, when households attempt to reduce debt through lower consumption in the aggregate, income decreases and the debt burden grows larger. The nature of this aggregate reduction in consumption is generally referred to as the “Paradox of Thrift” (a topic I’m told both Keynes and Hayek agreed on).

Having already written off massive losses on previous loans, private banks remain cautious in extending credit to households. Even though households have been deleveraging for 4 years, it will take at least another 4 years at the current pace to simply return debt levels to those existing in 2000. Returning to levels that preceded the Great Moderation may require another decade or more.

For the past several decades, private credit expansion has been the primary driver of economic growth. Government interventions, namely deficits, have been large enough the past few years to stabilize growth at a low level. If deficits continue to trend lower in the next couple years, the continued household deleveraging will once again spark fears of deflation. Given that current laws are already extremely supportive of private credit expansion, it’s hard to envision changes that would suddenly turn the tide. High inflation probably will return some day, but that day is a long way off. For now, disinflation remains the primary trend and deflation may still occur in the next few years.

Related posts:

Saving is NOT Enough for Consumer Led Recovery

Deflationary Monetary Policy

No comments:

Post a Comment